2018 should be a big year for climate mitigation in New Zealand as three factors converge: the potential for a Zero Carbon Act, continuously rising emissions and a growing sentiment for action from the public.

To cut emissions we need to stop investing in fossil fuel infrastructure and invest instead in renewable energy infrastructure. While all countries struggle with this, Australia and the US, for example, are closing coal plants and investing in solar and wind. This builds clean energy industries and creates expertise which can be a base for further progress in the future. In New Zealand there are no large commercial solar farms, no large wind farms are planned (the last moderately-sized wind farm to be constructed was Meridian’s 60MW Mill Creek, in Wellington in 2014), while Contact and Nova are renovating and building gas power stations. Indeed, in the present policy environment, unless demand grows, why would an existing generator build a wind farm? Adding a wind farm would lower the wholesale price of electricity and potentially leave all generators worse off.

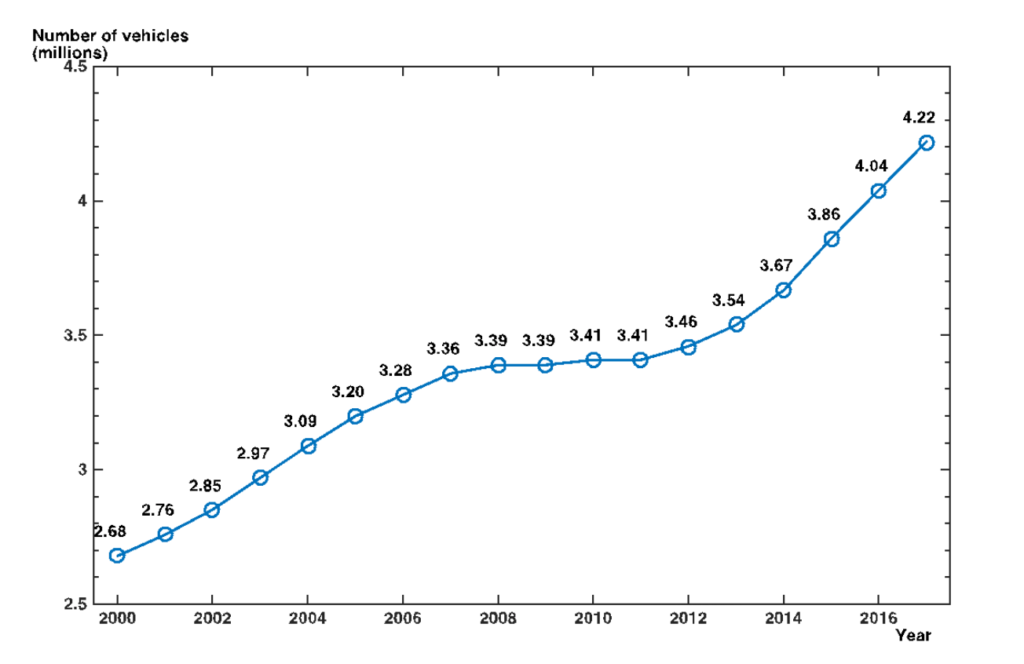

But let’s talk about cars. The car importing business represents a huge, ongoing malinvestment in fossil fuel infrastructure which we must face head on. The 325,000 petrol and diesel cars imported to New Zealand last year will be emitting greenhouse gases for many years to come. Worse, the total number of cars is increasing rapidly – a development that took many people by surprise, after an apparent plateau during the GFC (there were even articles at that time about how young people preferred to buy a smartphone than a car). The climate only cares about cumulative emissions, but at the moment it is not clear how we can compensate for our cumulative transport emissions, since 2000, say. In the past three years we’ve been adding 183,000 vehicles (almost all of them cars and small commercials) to the fleet per year. Aucklanders can guess where most of them have ended up.

Number of vehicles in New Zealand, 2000-2017. Source: NZTA. Credit: Environmental Health Indicators New Zealand. This represents one of the highest ownership rates in the world (compare our 4.22m vehicles to our 3.7m adults).

CO2 is invisible; the damage in extracting, processing, and burning oil is often far away and invisible. But cars are not invisible. They are very much in your face, every day for most of us, especially in our cities that are now completely choked with cars. You can’t turn on the TV for five minutes without seeing an ad for an SUV or sports car. For most of us the car is our single greatest source of personal greenhouse gas emissions.

Many believe that electric vehicle technology (EV, including both full electrics and plug-in hybrids) is superior to the internal combustion engine vehicle (ICEV). It cuts local emissions significantly — by 90 percent today, and by more tomorrow as we move to 100 percent renewable electricity. Techno-optimists can point to Tesla, to the trickle of EV models becoming a flood, to massive investments by old and new car manufacturers. They see EVs becoming cheaper, with longer range and complete charging networks. At this point EVs will be winning on all points and the revolution assured. There may be a rapid ‘S-curve’ adoption like that of the smartphone.

I am not so sure.

First, progress around the world has been extremely variable to date.

Here are the market shares of EV sales, as a percentage of total sales, in three leading markets, Norway, Iceland, and Sweden, all three doubling every two years or less:

| 2013 | 2014 | 2015 | 2016 | 2017 | |

| Norway | 6% | 14% | 23% | 27% | 34% |

| Iceland | 0.9% | 2.7% | 2.9% | 5.7% | 13% |

| Sweden | 0.7% | 1.7% | 2.6% | 3.2% | 4.7% |

Market share of electric vehicle sales, as a percentage of total sales.

Now for three very large markets that have been trying hard, the UK and Germany (doubling every two years) and the US (doubling every 5 years).

| 2013 | 2014 | 2015 | 2016 | 2017 | |

| UK | 0.2% | 0.6% | 1.1% | 1.5% | 1.9% |

| Germany | 0.2% | 0.4% | 0.8% | 0.8% | 1.6% |

| US | 0.6% | 0.7% | 0.7% | 0.9% | 1.2% |

Market share of electric vehicle sales, as a percentage of total sales.

Optimists foresee a worldwide doubling of market share every two years, reaching 60 percent by 2030; after that, bans on the sale of ICEVs are more prevalent, and the transition could largely be complete by 2040. Heavy transport follows close behind and 60 percent of oil consumption could be gone by 2050.

But consider one very sad story, Denmark, a country of 6m people and a renewable energy leader in Europe, which has experienced mixed results with their EV policies:

| 2013 | 2014 | 2015 | 2016 | 2017 | |

| Denmark | 0.3% | 0.9% | 2.3% | 0.6% | 0.4% |

Market share of electric vehicle sales, as a percentage of total sales.

Tax on new vehicles, previously 180 percent, had been waived for EVs. From 2016 the tax was reduced to 150 percent for ICEVs, while the EV tax was raised to 20 percent in 2016 and is being phased in to 150 percent by 2022. Despite the high tax, Denmark still has some the highest per-capita car sales in Europe.

Another perplexing example is the Netherlands, which also has sizeable (but fluctuating) incentives, as well as the most extensive charging network in the world, but no clear signal of accelerating adoption:

| 2013 | 2014 | 2015 | 2016 | 2017 | |

| Netherlands | 5.6% | 3.9% | 9.6% | 6.0% | 2.2% |

Market share of electric vehicle sales, as a percentage of total sales.

Second, the EV transition may need more help to become a reality.

The first six countries above all have complex and widespread incentive systems in place. Norway provides an effective discount of about 1/3 of the up-front cost, with other extensive ongoing incentives. The US provides a discount of up to US$10,000 and a gas guzzler tax (in place since 1978) of up to US$7700. The UK has a petrol excise tax of 58p/l (compare New Zealand’s 60c/l, the same in real terms as 50 years ago), an EV rebate of up to £8000, and no road tax for EVs—but up to £1120 + £515/year for gas guzzlers. Controversially, the UK road tax system was changed in April 2017, so far without ill effect on EV sales.

Third, getting the transition underway may require a change in attitudes.

Robert Llewellyn, host of the popular web series ‘Fully Charged’, remarked in his testimony to a parliamentary committee on EVs that he does not see the famous ‘S-curve’ transition as being in the bag by any means. People have a complex emotional relationship to their cars. They may stick to their favourite kind of car (or an emerging new one, like the huge SUV) beyond any obvious reason. I find it striking that in the EV world, most people want to talk up the amazing advantages of EVs; yet few want to dwell on the evil of ICEVs. I like to imagine public health information posted at petrol stations such as these:

This vehicle emits poisonous gases and you may be killing your neighbours by its operation.

This vehicle emits gases known to be damaging to the long term stability of the climate and estimated to cause trillions of dollars in damages.

The exhaust gases of this fuel remain in the air and oceans for thousands of years, raising sea levels and acidifying the oceans.

The product you are dispensing is directly responsible for major wars and terrorist attacks.

It may seem far fetched, but the public seems to accept analogous warnings on cigarettes. Why not on fossil fuel burning cars?

Some activists, such as Naomi Klein, would say that driving a petrol car is wrong. Arnold Schwarzenegger, who is suing oil companies for first-degree murder, would say that the manufacturers, importers, and sellers of cars, the producers and refiners and sellers and burners of oil, are in fact a public nuisance. And clearly, the Volkswagen emissions scandal ‘Dieselgate’, the ExxonMobil climate change denial controversy ‘ExxonKnew’, and some mining operations are wrong. But most of us are both actors and victims, caught in a difficult situation. Some car companies are clearly stalling, others are deliberating restricting the supply of ‘compliance vehicles’, but all of them need the income from selling ICEVs to fund the development of EVs, and they’re the ones with money and expertise. Just to pick one local example from many, Toyota NZ—a leader in the Sustainable Business Council and in greening their own operations—feels compelled to fill their ‘Sustainability’ page with subtle digs at all-electric vehicles, because Toyota doesn’t have one.

It’s a tautology that ceasing investment in ICEVs means not actually buying them anymore. Incentives, charges, advertising campaigns, are just mechanisms. Are people really ready for that to happen? In general terms, New Zealanders say they want the government to act on climate change but have we made the connection to our own behaviour and the current freedom to pollute? We’re talking about changes coming that will make the extra 10c/l in the pipeline for Auckland look like spare change.

Fourth, time is running out, both for the planet and for our goals.

A Zero Carbon 2050 Act is coming this year. That’s 32 years. Planting trees will buy us some time, but let’s regard them as offsetting agricultural emissions. CO2 should see steeper reductions than methane, and many industries will need ongoing protection while acceptable reduction plans are set in place globally. (There’s no point closing one of the world’s cleanest smelters, Tiwai Point, when China is building coal-fired smelters flat out.) Some sectors, such as aviation, have no low-emission options yet. What’s left? Private cars! The alternative exists already; the emissions savings are large; there is no local car industry to protect or cajole; while cars have some productive value, they are by and large consumer items; the NZ$8.4b a year we spend importing vehicles is a valuable existing source of finance that can fund the low-emission transition; the NZ$5b a year we spend importing fuel is a pointless ongoing drain on the current account. As the transition gets underway, the fuel savings will grow rapidly.

The actions required for the scale and speed of the transition could be large. One proposal currently gaining attention is a feebate, developed in depth by Barry Barton and Peter Schūtte in a November 2015 report. A feebate is charged on every newly imported vehicle that is directly related to its emissions. In the simplest model, the feebate varies in direct proportion to emissions and adjusted so that the entire scheme is revenue neutral. Let’s consider an example. (The actual dollar amounts can be scaled up or down depending on what is needed.) Buyers of a gas guzzler like the biggest 240g/km Toyota Hilux or Mercedes might pay an extra NZ$4000 up front. Buyers of smaller cars like the 140g/km Honda Civic or the 110g/km Toyota Yaris might get rebates of NZ$2000-3500, while 17g/km EVs get a rebate of NZ$9,000. The amounts would change over time as the fleet gets cleaner. The difficult question, not answered here, is the overall scale of the scheme. With these numbers — broadly similar to what other countries are already doing — NZ$300m is changing hands per year. Not a small sum, but not as big as the NZ$13b spent last year on vehicles and fuel. At some point, the scale of the scheme has to be pegged to the market response.

The Barton-Schūtte proposal achieves emissions reductions in one area — cars. That goes against decades of official thinking in New Zealand, which is that a single price for carbon may decarbonize the economy at least cost. This kind of thinking has to go. Not only is it not necessarily true, it flies in the face of the reality that (a) our emissions are rising, not falling, and (b) we don’t have a fixed price for carbon anyway; there are all sorts of exemptions and allowances in place. Andy Reisinger, of the NZ Agricultural Greenhouse Gas Research Centre, wrote in submission to the Productivity Commission that:

“I disagree… that direct regulation doesn’t achieve emission reductions at overall least cost to the economy. That statement would only be true if there were no market failures, no information limitations or asymmetries, and no preferences in specific interest groups that go beyond economics… It is also important to consider whether least-cost is the dominant criterion for policy choices, or whether risk, equity, social inclusion etc. are not equally or more important”.

Even the Australian government, so far no EV hero, is now considering direct regulations that would cut emissions of new cars 45 percent by 2025.

So 2018 really is shaping up to be a big year. As the groundwork takes place for the Zero Carbon Act and the Climate Commission, there will be plenty of opportunities to talk about cars.

Leave a comment